Rental Car Insurance Basics Explained

Rental car insurance is simply a set of coverage options designed to protect you financially if something happens to your rental vehicle—think accidents, theft, or even a cracked windshield. It’s an easy add-on at pickup, but whether you actually need every coverage offered can be confusing for many travelers. When I first rented a car, I wasn’t sure if my own car insurance or credit card would cover any damages, which made the rental counter offers feel overwhelming.

Here’s where many renters get stuck: do you need the rental company’s loss damage waiver, liability protection, or both? The answer really depends on what protection you already have. Some auto insurance policies extend coverage to rental vehicles, especially in the U.S. Many major credit cards offer some form of collision or damage coverage if you pay with the card. If you skip these checks and just accept everything at the counter, you might end up spending more than needed—sometimes doubling your daily cost.

I usually recommend reviewing your personal car insurance policy or asking your credit card provider about their benefits before you even start browsing rentals. That way, you can decline unnecessary add-ons with confidence and keep your trip budget in check. Plus, planning both your flight and car rental together—like on the airtkt.com car rental booking page—can help you see your full trip costs upfront.

Understanding Rental Car Insurance Options

Sorting out insurance options at the rental car counter can be overwhelming, but knowing what each coverage actually does—and doesn’t—include will help you avoid surprises on your trip. Here’s a breakdown of the most common types you’ll see when renting, including what they typically cover and what you’ll usually pay.

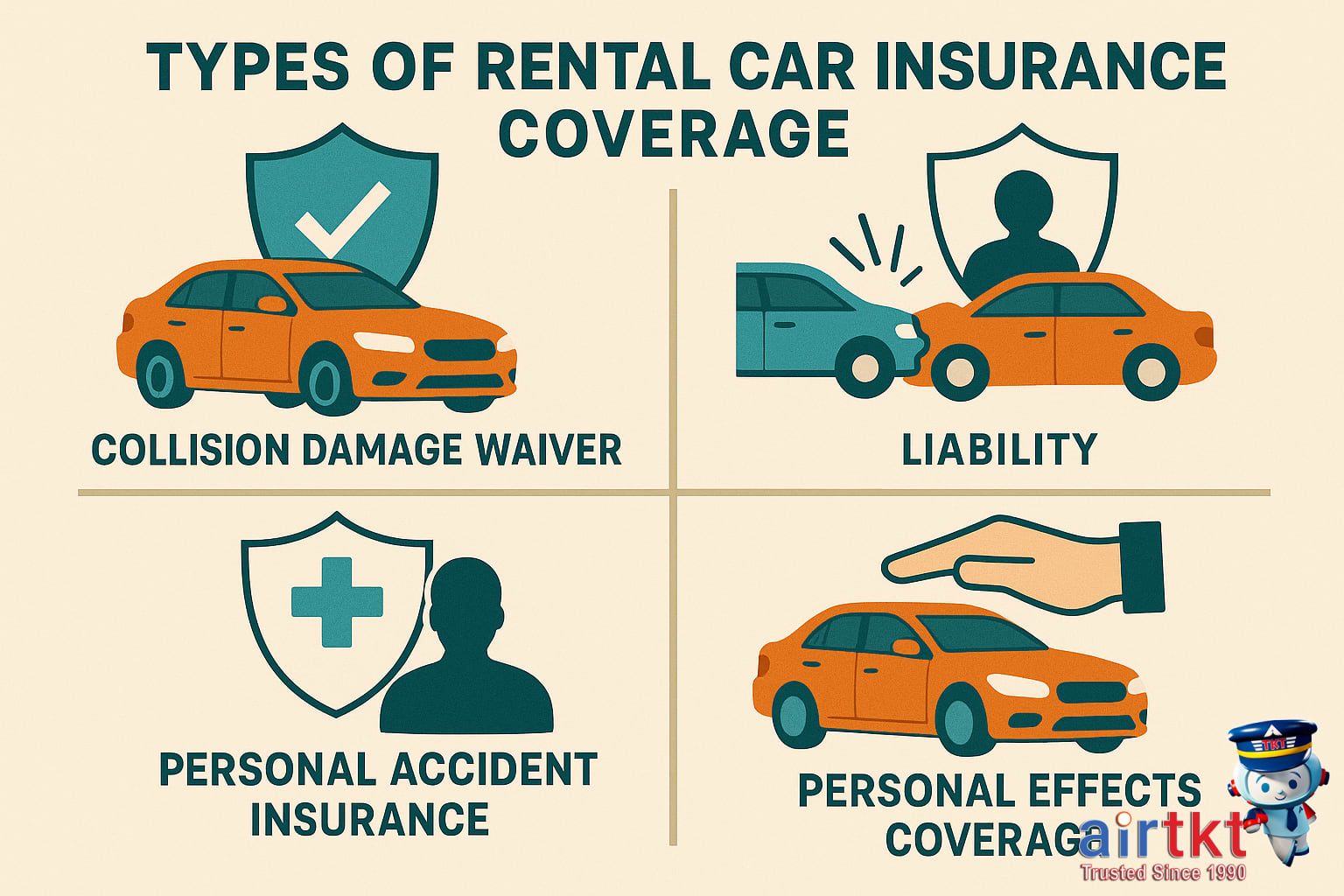

Collision Damage Waiver (CDW)

CDW, sometimes called Loss Damage Waiver (LDW), is not technically insurance, but rather a waiver that limits your financial responsibility for damage to the rental car, such as if you’re in an accident or the car is vandalized. I was surprised to learn CDW often excludes damage to tires, windshields, or the car’s underbody—so it definitely pays to read the fine print before accepting or declining. On average, expect to pay about $15.00 per day for CDW in the U.S., though this can vary by location and car class.

Liability Insurance

This coverage protects you in case you cause damage to other people’s property or injure someone while driving the rental car. In some destinations, basic liability is included in the rental price, but in others (especially outside the U.S.), the limits are quite low and you may want supplemental insurance. Supplemental liability coverage typically costs about $10.00 per day.

Personal Accident Insurance (PAI)

PAI covers medical expenses for you and your passengers in the event of an accident while using the rental car. If you already have health insurance that covers injuries abroad or if your credit card offers rental coverage, you might not need this extra layer. If you do purchase PAI, it usually runs about $7.00 per day.

Theft Protection

Theft Protection covers loss or damage to the rental vehicle due to theft or attempted theft. Sometimes this is bundled with CDW, and sometimes it’s separate—especially in international locations. Expect pay around $8.00 per day for Theft Protection if it’s offered as a standalone option.

If you’re comparing rental quotes through airtkt.com, take a few minutes to review which protections are legally required, what your own auto or travel insurance may already cover, and which add-ons actually make sense for your trip. Understanding these choices up front can save you money—and stress—at the rental desk.

How Credit Cards Cover Rental Insurance

Many credit cards come with rental car insurance as an included perk—often covering damage due to collision or theft when you use the card to pay for your rental. This benefit can be a real money-saver, but the actual coverage and conditions can vary quite a bit depending on your card.

Most cards offer what’s called “secondary coverage.” That means you’ll need to go through your own car insurance policy first if anything happens, and the credit card coverage only picks up the leftovers. However, a handful of premium credit cards offer “primary coverage”—so the card’s insurance kicks in first, which could save you from making a claim with your own insurer. In practice, I’ve found it’s crucial to know whether your card is primary or secondary; not checking this detail could come back to haunt you if you have an accident overseas.

Geographic restrictions are another important point. Some credit cards exclude certain countries or cap the length of coverage (often around 15–30 days). Places like Ireland, Italy, or Australia are often excluded, so don’t assume you’re protected everywhere just because your card promises rental coverage. Also, most credit card insurance will cover the car itself but not liability or personal injury.

I always double-check my card’s fine print to avoid surprises at the rental counter. You can usually find the details by logging in to your card’s online account or searching for your card’s “guide to benefits.” If anything’s unclear, a quick phone call to your card’s customer service team can clarify whether you need extra insurance or if your trip destination is covered. For more tips on using credit card perks wisely, check out the credit card benefits guide at airtkt.com if you’re doing more trip planning.

Choosing Right Rental Coverage

Sorting out car rental insurance can feel like a maze, but focusing on your trip details and personal situation helps you steer through. I’ve learned that assessing things like trip length, where you’re headed, and your own existing insurance is key. For example, on a short weekend trip, I skipped the personal accident insurance (PAI) because my health insurance at home provided solid coverage.

Factors That Matter Most

Your rental coverage needs will depend on several variables:

- Trip Duration: Longer trips might justify more coverage since you’re on the road more and exposed to higher risks.

- Destination: Local laws and risks differ—some international locations may require specific insurance like Collision Damage Waiver (CDW).

- Vehicle Type: Renting a luxury car? It might make sense to pay extra for enhanced coverage, but for a compact car you might stick with basics.

- Driver Age: Younger drivers, often under 25, may face extra fees or insurance limitations from rental companies.

Evaluate these before you reach the counter. If your credit card covers collisions or theft, for instance, you might skip CDW and save a chunk of change. On the flip side, if driving in a country with high accident rates (or strict laws), extra protection could spare you stress.

Essential vs. Optional Coverages

Typically, liability coverage is a must—often required by law or included by the rental company. Collision Damage Waiver (CDW) and Theft Protection are wise if you don’t already have them through your personal auto insurance or credit card. Extras like Personal Accident Insurance (PAI) and Personal Effects Coverage are easy to skip if your existing health or homeowner’s insurance handles these risks.

Always review what your current policies or credit cards actually include before you fly, as coverage definitions and exclusions vary. It’s also smart to call your issuer directly and confirm details you’re unsure about.

Bring Documentation for Peace of Mind

Rental agencies sometimes require proof of your existing insurance or credit card coverage, especially if you decline their options. Bring a copy of your policy or a letter from your card provider. I’ve found that having my documents ready speeds up the pickup process and avoids awkward debates at the counter.

Rental Car Insurance Budget Table

When you’re mapping out expenses for a trip, it’s easy to focus on flights or hotels. But in my experience, rental car insurance can be a real wildcard in your total spend. Set aside a clear chunk for insurance and you’ll likely avoid unplanned costs or last-minute surprises—a lesson I learned after comparing insurance totals with my other trip expenses.

The overview below gives a practical breakdown of estimated daily costs for three different budget styles—including accommodation, food, transport (with a spotlight on insurance), and activities. Use it as a starting point to align your own plans or reference more detailed AirTkt travel budgeting tips or rental car deals for extra savings. Note that in the “Transport/Insurance” row, the price represents an average rental car cost per day, including typical insurance bought via the rental desk or online aggregator.

| Budget | Mid-range | Luxury | |

|---|---|---|---|

| Accommodation | $40.00 | $85.00 | $210.00 |

| Food | $20.00 | $45.00 | $100.00 |

| Transport/Insurance | $28.00 | $55.00 | $110.00 |

| Activities | $15.00 | $35.00 | $85.00 |

Rental car insurance can account for a good portion of your daily transport costs, especially at the mid or luxury level, so adjust this line item before committing to activities or restaurant splurges. Don’t leave insurance as an afterthought, since even a small difference multiplied by several days adds up quickly.

Common Rental Insurance Questions Answered

- Do I need CDW if my credit card offers coverage?

In many cases, credit cards provide Collision Damage Waiver (CDW) coverage, but you’ll need to decline the rental company’s CDW at the counter. Double-check your card’s benefits beforehand, as some only cover secondary insurance or limit coverage by country. I’ve found calling my card issuer saved me from buying unnecessary coverage on past trips.

- What liability insurance is typically required?

Most car rentals include a minimum liability insurance policy, which covers injury or property damage to others. However, these limits often meet only local legal requirements. For extra protection, consider supplemental liability insurance, especially if you want coverage beyond basic requirements in case of a more serious accident.

- Is rental insurance mandatory for international drivers?

Rental companies usually require some proof of insurance if you’re an international driver. If your home auto policy or credit card doesn’t provide rental coverage abroad, it’s smart to purchase coverage directly from the rental agency. This avoids the risk of denied claims due to policy exclusions for international rentals.

- What damages does rental car insurance not cover?

Rental car insurance often doesn’t cover damage from off-road driving, lost keys, interior stains, personal belongings, or driving under the influence. For instance, if you leave valuables in a parked car and they’re stolen, most policies will not reimburse you. It pays to know these exclusions before you drive away.

- Does my travel insurance cover rental cars?

Some travel insurance policies include rental car protection, but details vary widely. It’s common for this coverage to only apply to vehicle theft or certain types of damage, not third-party liability. Always review your policy’s rental car section, and check for country restrictions or claim documentation requirements before relying on it.

- What should I do after a rental car accident?

If you’re involved in a rental car accident, contact the local authorities, document everything with photos, and notify the rental company right away. Get a copy of the police report if possible. Fast action helps avoid complications with both insurance claims and the rental agency after your return.

Finalizing Smart Insurance Choices

Wrapping up your car rental insurance planning doesn’t have to feel overwhelming. Let’s run through the main lessons from this guide: you’ve now explored rental agency policies, gotten a handle on credit card coverage, and learned how to factor insurance costs into your travel budget. Double-checking these details really pays off—I know I felt much more prepared and even saved a noticeable amount on my last trip after using these strategies.

Main takeaways? Understand exactly what your primary and secondary insurance options cover. Never assume your credit card will fill all the gaps—terms change, and coverage can vary quite a bit between cards and destinations. That’s why, before you sign any rental agreement, it’s vital to confirm your coverage specifics directly with both your card issuer and rental provider. I always recommend asking for written confirmation, so there’s no confusion later on should you need to make a claim.

Budgeting for insurance is often overlooked, but knowing the precise coverage you’re paying for means fewer unexpected expenses at the rental counter. Use your trip research to determine whether buying extra coverage makes sense for peace of mind, especially if you’re driving in unfamiliar territory or want to avoid out-of-pocket costs.

If you’re ready to simplify your next rental car booking, don’t forget you can compare options on the airtkt.com rental car page. Having everything in one place makes it easier to match your insurance needs with the best rental deals.